401(k) Plan Sponsor Services (3(21) Co‑Fiduciary) in Atlanta

A better 401(k) for your people—built for fiduciary excellence

Transparent fees, prudent investments, and real employee education—without overloading HR.

-Role: ERISA 3(21) co‑fiduciary

-Focus: Prudent lineup, documented governance, measurable employee outcomes

Request a no‑cost fee & design diagnostic

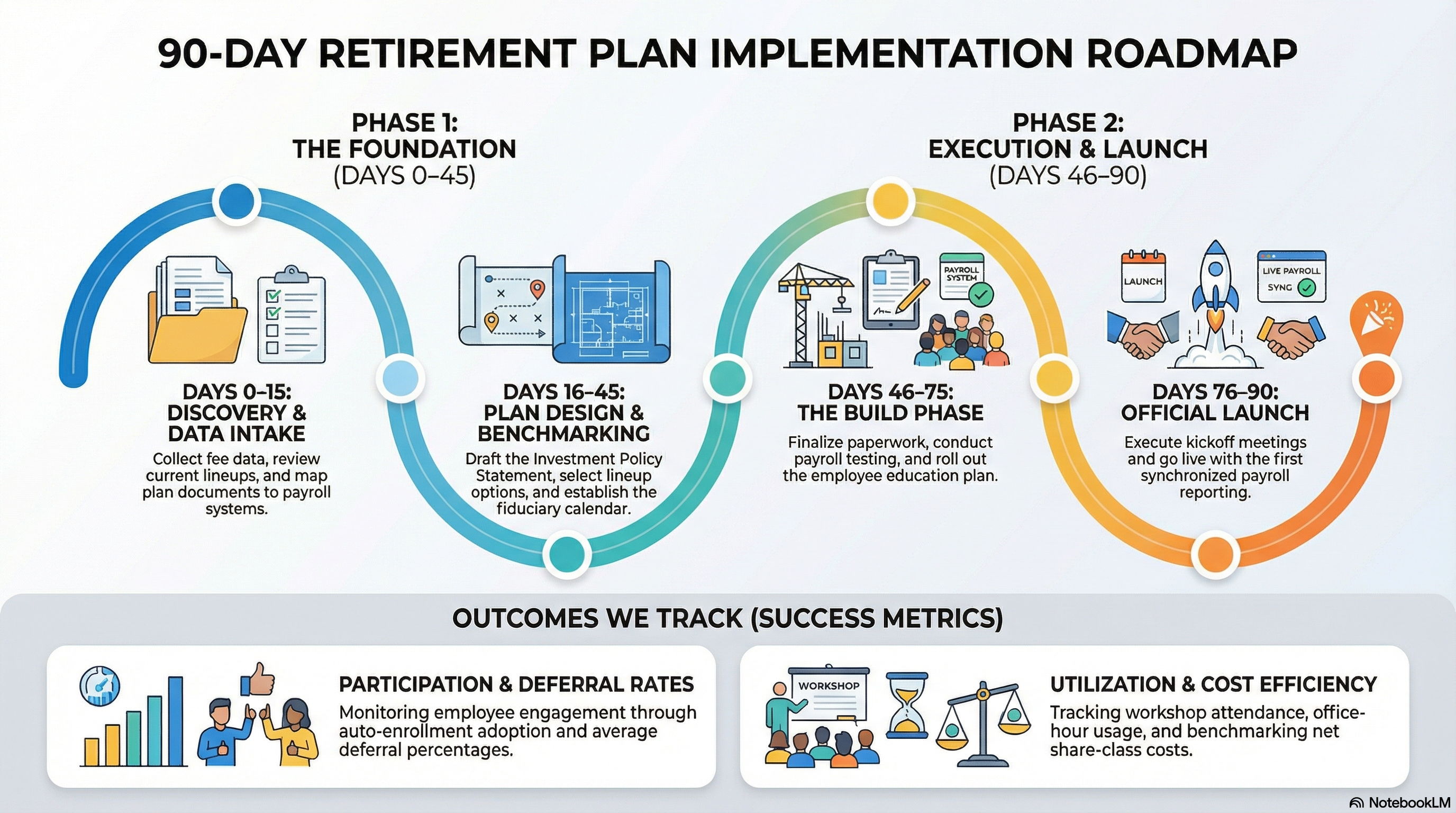

What you get

Our fiduciary role

- Lock Wealth Management serves as an ERISA 3(21) co‑fiduciary. You retain final decision‑making authority; we provide prudent, documented recommendations and ongoing monitoring. Prefer to delegate decisions? We can discuss a 3(38) option via a discretionary partner.

Provider‑agnostic coordination

- We are agnostic and will guide your plan based upon service quality, technology, fiduciary support, investments options and payroll integrations. Pending review, we retain the current service providers or discover options for providers that may be a better fit. If you are starting a new plan, we have resources with all plan service providers to ensure your needs are met.

Pricing (clear and flexible)

- Structure: Blended, asset‑based advisory fee with flat and hybrid options available

- Typical ranges: Most small–mid sized plans land between 0.20%–0.75% annually, disclosed under ERISA 408(b)(2) and benchmarked each year

- Minimums/caps: Applied as appropriate and shown in your proposal

- Bundle note: Employee Financial Wellness is a separate service; bundle pricing is available for 401(k) clients. We disclose all compensation under 408(b)(2) and review fee reasonableness annually with your committee.

Or book a 15‑minute fit call

Looking for workforce education? Visit our Employee Financial Wellness program.

401(k) Plan Sponsor FAQs

Are you a fiduciary to our plan?

Yes. We serve as an ERISA 3(21) co‑fiduciary—you retain discretion; we provide prudent, documented recommendations and monitoring. If you prefer discretion delegated, we can discuss a 3(38) option via a partner.

How do you charge for 401(k) advisory?

We use a transparent, blended asset‑based schedule, with flat and hybrid options available. Most plans fall between 0.20%–0.75% annually, disclosed under 408(b)(2) and benchmarked each year. Minimums/caps may apply and are shown in your proposal.

Do you work with our current recordkeeper/TPA/payroll?

We can work with any TPA/Recordkeeper/Payroll and unlike many advisory firms (wirehouse and Brokers); we don’t require a selling agreement with any service provider. This positions Lock Wealth Management to have our clients’ best interests as priority

What employee education do you provide?

Workshops, office hours, and targeted communications aligned to plan milestones. We track participation, deferrals, and engagement and review results with your committee.

Do you help with employer‑sponsored 529 plans?

Yes. We include a concise 529 education module alongside our 401(k) communications to help HR enable payroll contributions and educate employees. Employer benefits: Stronger total‑rewards story, low‑lift implementation (payroll + education), supports recruiting/retention. Employee benefits: Tax‑advantaged growth, potential state tax deductions/credits (state‑specific), easy payroll contributions. If funds aren’t used for college: Under current law, certain unused 529 balances may roll into the beneficiary’s Roth IRA within limits (e.g., 15‑year account age, annual IRA limits apply, lifetime cap currently $35,000).